When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

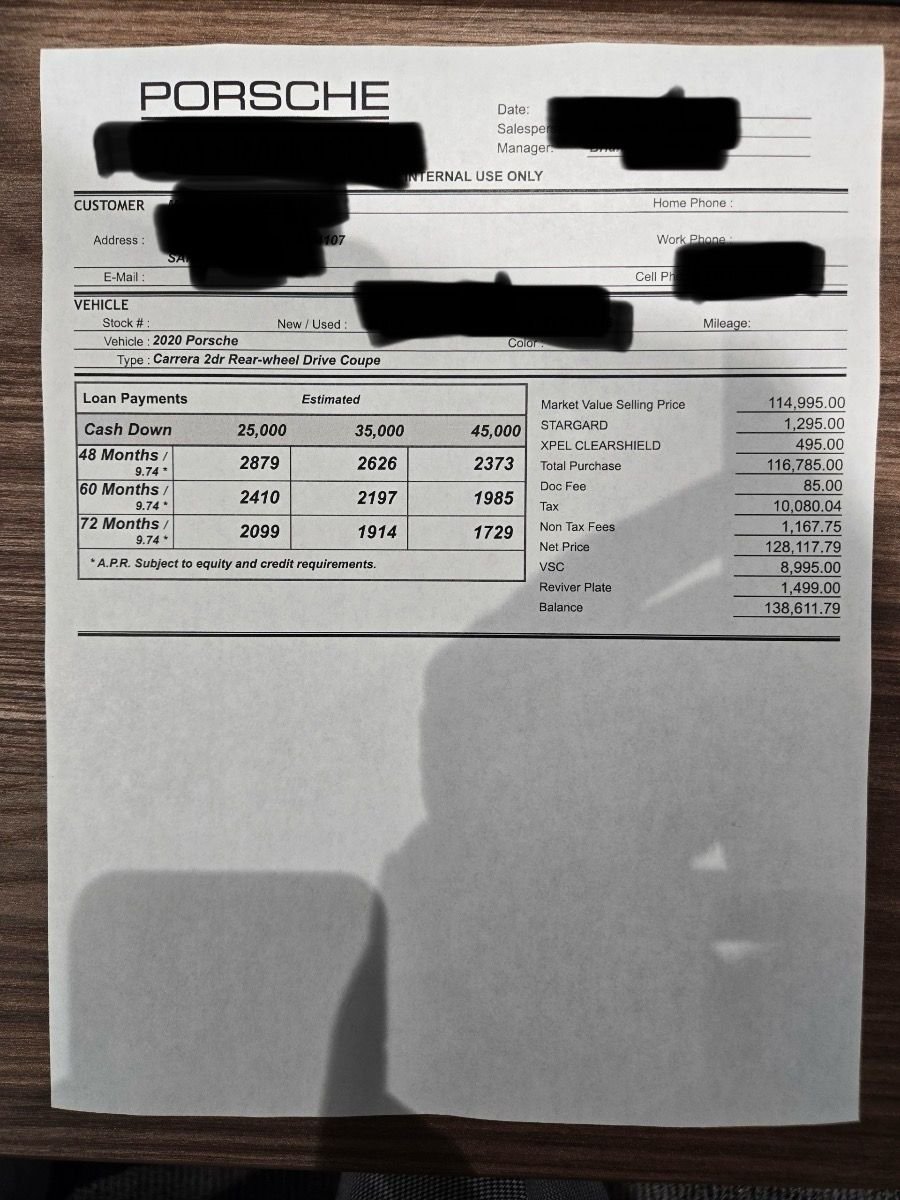

What are the most ludicrous offers you've received from a dealer? I got this one yesterday on a base 2020 992 with 17k miles and $120k MSRP. $3k+ in useless add-ons and $9k for a VSP on a CPO (??!!!)... on top of sale price that's already ~$5k+ above market. Great way to lose my business indefinitely. Bay Area dealer.

Bay Area dealer. The only surprise here is that you would be surprised. You're going to pay top dollar in the bay.

When you're financing, they'll push a service contract, because they're presuming that you're extending yourself to buy the car -- you may be scared of service costs or simply want to finance the service. Fair or unfair assessment, you don't have to do it.

You don't have to take all of the things that they put together on the offer. People seem to forget that these things are indeed negotiable. There's no need to be indignant, you can always counter. Indignation gets you nowhere. If the deal isn't working for you, no drama necessary. My son has witnessed me shake hands, say no thank you, get up/walk to the door -- and the right deal magically happened.

The proposed financing raises an eyebrow to see the same rate for 3 different loan terms. Higher rates are to be expected when you're financing a used car. You should have gone in with a pre-approval from a lender and give the opportunity for the dealer to beat it. The biggest most adult leap that a car buyer can make is to walk onto that dealer lot already knowing how they're going to pay for the car.

I am going to get on my soapbox and say that if the difference between a 60 and 72 month term is the difference between you being able to afford or not afford the car, you can't afford the car. IMHO, 60 month is the upper limit already. In a higher APR environment, you really want to live in 48 month land (better yet, cash), because wow, does 10% APR add up over a longer loan term.

Admittedly, I have a mental block around financing a used car. Not only will that interest add up, but you won't have this thing paid off until it's an 8-10 year old car. Depreciation does indeed happen at that age and the actual cost of owning the thing between used car loan interest, depreciation, and maintenance is consequential.

As noted above, counter-offer with the deal that you want. The worse that they can say is no. No drama. Put forth the deal that you want to do. Oh, and if you're doing this, secure other financing, because their proposal is DOA and not worth the credit pull.

Bay Area dealer. The only surprise here is that you would be surprised. You're going to pay top dollar in the bay.

When you're financing, they'll push a service contract, because they're presuming that you're extending yourself to buy the car -- you may be scared of service costs or simply want to finance the service. Fair or unfair assessment, you don't have to do it.

You don't have to take all of the things that they put together on the offer. People seem to forget that these things are indeed negotiable. There's no need to be indignant, you can always counter. Indignation gets you nowhere. If the deal isn't working for you, no drama necessary. My son has witnessed me shake hands, say no thank you, get up/walk to the door -- and the right deal magically happened.

The proposed financing raises an eyebrow to see the same rate for 3 different loan terms. Higher rates are to be expected when you're financing a used car. You should have gone in with a pre-approval from a lender and give the opportunity for the dealer to beat it. The biggest most adult leap that a car buyer can make is to walk onto that dealer lot already knowing how they're going to pay for the car.

I am going to get on my soapbox and say that if the difference between a 60 and 72 month term is the difference between you being able to afford or not afford the car, you can't afford the car. IMHO, 60 month is the upper limit already. In a higher APR environment, you really want to live in 48 month land (better yet, cash), because wow, does 10% APR add up over a longer loan term.

Admittedly, I have a mental block around financing a used car. Not only will that interest add up, but you won't have this thing paid off until it's an 8-10 year old car. Depreciation does indeed happen at that age and the actual cost of owning the thing between used car loan interest, depreciation, and maintenance is consequential.

As noted above, counter-offer with the deal that you want. The worse that they can say is no. No drama. Put forth the deal that you want to do. Oh, and if you're doing this, secure other financing, because their proposal is DOA and not worth the credit pull.

I hear you on all of that and thank you for the thoughtful response. The issue here is the bid/ask is too ridiculous. The most I'd pay for this car is $105k + doc fee + taxes. That is $20k shy of their ask. Based on my experience with other Bay Area dealers, the "add-ons" are non-negotiable ("it's already installed, my hands are tied"). Will be looking to ship from elsewhere...

As with any deal, if you start too aggressively, there's no point in wasting time countering!

I don't feel comfortable saying, but it's 2 letters that starts with S and ends with F

I live in SF and have been to many of the dealerships (currently building a TT with Porsche Walnut Creek). Just based on your description, I knew it was likely SF. I have found them completely unenjoyable to work with. I�ve greatly enjoyed WC as well as Marin.

I live in SF and have been to many of the dealerships (currently building a TT with Porsche Walnut Creek). Just based on your description, I knew it was likely SF. I have found them completely unenjoyable to work with. I�ve greatly enjoyed WC as well as Marin.

I went to the dealer to trade my 2023 911 Cab.with only 6000 miles and they only offered me $125,000. They always beat people up on the trades then turn around mark it up. I know they have to make money and I don't have to trade.

I went to the dealer to trade my 2023 911 Cab.with only 6000 miles and they only offered me $125,000. They always beat people up on the trades then turn around mark it up. I know they have to make money and I don't have to trade.

As someone else said, it's as if they're in the business to make money. Of course you will get offered a bit less for your trade-in than what they advertise for. The actual used car purchase price will be lower than what we see in the marked up published price, they have the cost of holding the car, they have to pay the used car sales commission, and they run the risk of getting screwed if the used car market changes for the worse and the car doesn't sell.

Don't trade-in if you want the best money for your used car and it bothers you that they will turn around and sell it for more. Trade-in is a convenience and in some states (not mine) a tax benefit.

FWIW, please post who the dealers are as it's the only way for any of this to be helpful to the community. To simply say, they included a $300 fee to grease the retractable mirrors is perhaps amusing, but if it helps someone steer clear of a true $tealership that's another reason this site rocks!

You don't want to mention the dealer then be really safe and don't post at all.

The problem is the reaction to the offer by the OP.

Agreed....

31 Porsche dealers in California....none are offering a CPO 992 for $105K....especially when a 2020 992 has a current Trade-in value in the mid to upper $90K range.

Is the OP upset with this Porsche dealer or just any dealer that may view these types of inquiries as unrealistic?

07-09-2024, 07:37 PM

07-09-2024, 07:37 PM