When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

Long time lurker here; I have about 12 months left on my bmw M4 lease and I have been patiently waiting for my turn-in so I can finally get my dream 911. I've been doing a lot of research for the past few months and always checking local Porsche dealership websites to get an understanding of my options for when I do decide to get my 911. One of the major and obvious reasons that people don't lease 911's is because the finance payments are very similar to the lease payments. I've always been a leasing guy and I think I prefer it for my 911 just because I have to deal with less headaches, even though I'm "wasting" it all away after three years. I've never considered it a waste because I truly love driving my cars. The main question I have for the 992 members and Porsche guys in general is, on a 140k build what should I expect to be paying? There's a 146K MSRP 2019 911 Carrera 4 GTS as a lease special here in LA for 10k down, 1699 (pre-tax) a month and 5k miles/yr. When I went to my dealer a few days ago I think I was looking at 25k down 2200 a month for a C2S with an MSRP of 140K. I know leases obviously vary but the first 2019 GTS lease seems a lot more attractive to me. Am I getting shafted for the price my dealer gave me or is that the general idea for the new 992's? I'm just trying to get an idea of what I'll be having to pay for my dream car so any insight is appreciated as well as what kind of deals you guys got on your 992's

Lease payments have way too many variables - greedy dealers playing with money factors, how hot the car is in your market and what they're willing to discount, if the car is a demo/loaner/has miles, what current MF is from not only Porsche but other banks, and of course, your credit.

What I can tell you is that $25k down + $2200 a month presuming 36 months and no tax included for a 992S is insane and makes absolutely zero sense. That's $104,200 in total payments for a $140k car. Plus tax presumably too? NOT a good deal.

BMW has practically turned into a car rental company. They heavily subsidize their leases. Mercedes does the same.

It makes zero sense to lease a Porsche 911. The numbers don�t work. The Aston Martin Vantage, which stickers for about the same price as a 911, is a substantially cheaper car to lease. Heck, under some conditions, a McLaren 570S or even a Lamborghini Huracan are a better lease deal than a 911.

If you want a 911, buy it. If you�re financing, the payments are basically the same as a lease, but you aren�t flushing your money down the toilet as you would in a lease. You�ll be in a much better position for your next car from a financial perspective.

@njcycleguy@detansinn thank you guys so much for your insight! it appears i will be stepping out of my comfort zone and purchasing the 911 instead of leasing. with an 800 credit score, what should I expect as far as APR goes on a 140k MSRP C2S? and is it better to put a big down payment when financing? it will be my first time financing a car, not sure why i've always tried to avoid it so much, haha.

Interest rate depends on how long of a term you want. Find the bank/credit union with the best rate. I always look at PenFed and Navy Federal first but you need to qualify.

@njcycleguy@detansinn thank you guys so much for your insight! it appears i will be stepping out of my comfort zone and purchasing the 911 instead of leasing. with an 800 credit score, what should I expect as far as APR goes on a 140k MSRP C2S? and is it better to put a big down payment when financing? it will be my first time financing a car, not sure why i've always tried to avoid it so much, haha.

Rates are low right now, so it�s a good time to do it. Lots of variables � too many count, but between 3-4.5% is the most likely range. Down payment can have an impact, so play with that as well.

Rates are low right now, so it�s a good time to do it. Lots of variables � too many count, but between 3-4.5% is the most likely range. Down payment can have an impact, so play with that as well.

Great, thanks so much! One more question, sorry to bother so much... you said that I'll be in a better financial position with financing a 911. Care to elaborate? I have a feeling I'll always switch out of cars within 2-3 years, I grew tired of my M4 after a year (it's an amazing car but I'm always scrambling for something new and better). I understand that at the end of the lease I'm left with nothing, but would that not also hold true over three years of ownership and 40-45k miles on a C2S?

The world doesn't operate on black and white. Research the gray areas - that's what all the great people do and compound on it.

Leasing and financing each has their merits. What you need to get to do is get the nitty gritty on it to see what best applies to your individual situation.

It's very easy to say "oh, A is bad and B is good..." but that's what the mere average will consider and is the recipe for mediocrity.

Do your research, but in general I can share that leasing holds these two major benefits: you like to drive a new car more frequently and avoiding repairs; you can utilize tax benefits if you lease.

Finally, residual is lower slightly as of today maybe 2-3% compared to the 991.2's. I have heard people paying around 2500, w zero down on a 150,000K car, 15k miles.

I'm no expert, but I do hope instead of shooting down a valid question, there is better help to come.

Is that still possible? I thought writing off a lease was much harder these days, especially a luxury car vs a work truck.

My 2 cents having leased BMWs in the past:

Upsides:

Leasing gives you piece of mind if you get in a fender bender - you turn the car in at the end an Porsche eats the massive loss in value.

Tax in some states is on the portion you lease not the whole car.

New car every 3 years.

Downsides:

Dealers can screw you on Money Factor, BMW MF is set by BMW and it used to be easy to find so you could tell if the dealer was marking it up. That's not the case anymore and Porsche is the same. In other words you could be paying a lot in interest even with good credit.

The residual on a Porsche is usually on the pessimistic side. My calc on the last lease deal I saw would have the car being worth an estimate 10k less than what is likely.

Porsche are more strict than BMW/Benz on lease return, much more likely to get charged for small defects.

With a high credit score you should be able to finance a purchase at 3.5% or even less. The leases tend to be on much worse terms, although the details can vary especially for small business owners and a “work” vehicle. Auto loans are a lot more flexible now than even a few years ago. Leasing can have some peace of mind advantages, but you can also get supplemental insurance on a purchase instead.

BMW has practically turned into a car rental company. They heavily subsidize their leases. Mercedes does the same.

It makes zero sense to lease a Porsche 911. The numbers don’t work. The Aston Martin Vantage, which stickers for about the same price as a 911, is a substantially cheaper car to lease. Heck, under some conditions, a McLaren 570S or even a Lamborghini Huracan are a better lease deal than a 911.

If you want a 911, buy it. If you’re financing, the payments are basically the same as a lease, but you aren’t flushing your money down the toilet as you would in a lease. You’ll be in a much better position for your next car from a financial perspective.

Perfectly said.

OP: I leased my last 16 cars (including 6 BMWs and other luxury brands - always 15k miles per year and 36 months and zero cap cost reduction) and it made financial sense for me in those cases - at this point I can run the lease numbers as fast and accurately as the finance person at the dealership. For my Tesla and the 992 I ran the numbers and it made no sense so I financed (plus in PA you pay an extra 3% sales tax on a car if you lease). For the 992 I put down $43k and financed about $105k at 4.64% interest (credit score 830 or so) - the dealership tried Porsche finance and four other banks to get the best rate. If you stay below $100k it might be a slightly lower rate.

As for tax benefits of leasing - my Alfa is my 'company car' that I leased through my company. Usual pros of leasing plus all costs come out of pre-tax income, but insurance and some other items are more expensive. Again I ran the number for finance, personal lease and business lease and the business lease came ahead slightly vs personal lease and way ahead of financing for that vehicle.

Talk to a few Porsche dealers - they want you to get the car so hopefully won't inflate numbers much. Alternatively find a car broker to get the best information for your needs.

You will have to find out what PFS set the money factor (interest rate) and residual (depreciation) for their cars for the month. Edmunds usually is a good source https://forums.edmunds.com/discussio...-all-models/p7

Here's an example from the above link for a some 2019 Carreras for a 3 year lease I believe.

You multiply the money factor by 2400 to get the interest rate, 6.96%. You multiply the residual by the MSRP (not negotiated price) to get the value of the car at the end of the lease, 0.57x$161,500 for the Targa, or $92,055.

The residuals for 2019 model year cars should be lower than 2020 models so that leasing the newest car should cost less than the older car. The quote that dealer gave you on a $140k 2020 Carrera assuming a 58% residual must have used a 12-15% money factor depending on if sales tax was included. If the money factor was at 7%, the payment excluding sales tax should be about $1500/mo with a $25k down payment which you should not do. It should be about $2200/mo with $0 cap cost reduction.

You can't negotiate the residual. You can negotiate the price and money factor down to PFS base rate. Dealers will get very vague with lease numbers trying to talk only in terms of your downpayment and monthly cost, but you will at least know how close you are to the best deal available to you.

With a high credit score you should be able to finance a purchase at 3.5% or even less. The leases tend to be on much worse terms, although the details can vary especially for small business owners and a �work� vehicle. Auto loans are a lot more flexible now than even a few years ago. Leasing can have some peace of mind advantages, but you can also get supplemental insurance on a purchase instead.

You didn't mention the upfront fees involved with leasing and financing (> $1K). I have never meet anyone that got rich by financing a car. Why would anyone buy insurance in case they get upside down on a loan?

Yes, the business use of a vehicle will trigger some tax deductions within an IRS Form "C" Corp or an IRS Form 1065 (a K-1 is issued). Those are limited by law to what a cheap Chevy 4-door may cost. There is never a tax deduction for an upgrade to a nicer car.

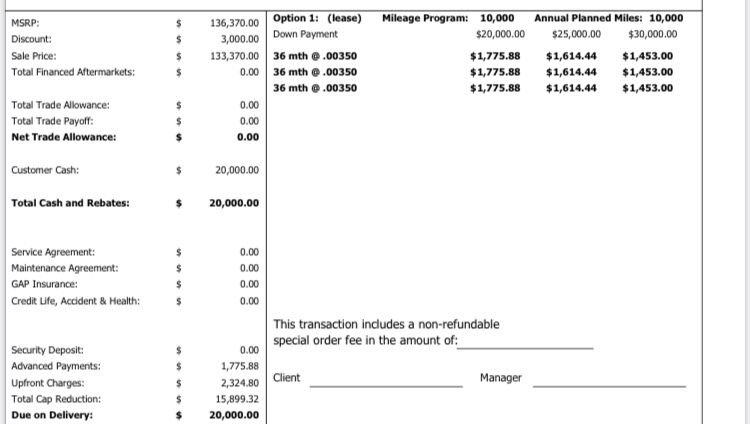

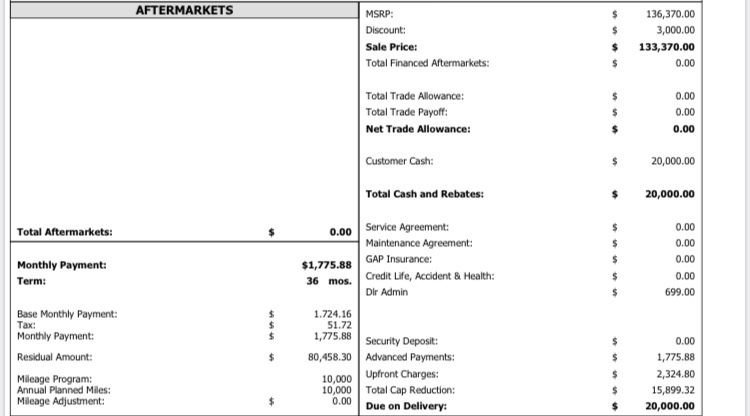

Here�s an example lease for a 992 with an MSRP of $136,370.00. Should contain all of the information needed to make an estimate of worth (MF, residual, ...). Use those numbers to calculate interest and so forth as suggested above. This is an initial offer/quote from a dealer in North Carolina; nothing has been signed.

11-10-2019, 11:13 AM

11-10-2019, 11:13 AM