When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

My car fund started at $30k in 1999. It has grown significantly both from injecting more cash and from market appreciation. At one point I took money out to put towards buying our current house. I am winding it down currently as I just have 1 bike left and I am done with old cars for now.

If I had $100k in it and wanted to buy a $125k car, I would do that as long as I was confident that I wouldn�t lose any of the $125k plus on-the-road expenses over the next 2 or 3 years. Most times, I have been right in my assumptions, but not always. I have a 1993 Harley right now that I have about $16k in. Looks like I might only get $10k out of it.

I started a small collector car dealership about 20 years ago when I was between jobs. It was called Collectible Investments. That is how I view collector cars. Somewhere to park capital with the ability to use it for fun. No real focus on growing the capital - it�s more about protecting the capital and using it without any real consumption. The use without loss is the growth I am looking for. if my daily depreciates, I don�t care as I have planned for that. If I lose on my car fund, I�m pissed off at myself.

I know what to buy from playing with collector cars for decades and sticking to the brands that I know. However, there are no guarantees with any market including collector cars.

My lease calculations are only to set reasonable/conservative payments for my home budget. Nothing that I am doing is for tax reasons nor do they offer any tax advantage. I do not own the business that I currently work for.

thanks for sharing. I think that I should follow your step and look into starting a smaller collector car dealership

FWIW I think you've gotten some pretty valuable advice from those who answered your question. Some very smart people here.

My more recent purchases included a 991.2 for which I paid cash and then I bought a new Cayenne Turbo (and also paid cash). I'm not bragging about money or any of that kind of BS I just figured these are toys or transport and if I can't afford to buy them that way I shouldn't. I have a very good financial advisor and most of our (my wife's and my own) money is very diversified- mutual funds, real estate, stocks and, lately, a lot of CDs. The latter can give you 5.4% without risk.

The Cayenne will deprecate like a stone, the 991.2 less so. But driving them gives me joy that I think is worth it. I plan to keep them for a long time hence I don't really care.

The first cars I bought made a lot of money for me. But I really can't think of any car in the current day and age that would do the same- unless you're investing in the millions. Unless I were buying early British, German or otherwise semi-undervalued cars I can't see any of them as an investment but just as things you can hold onto and enjoy and lose as little as possible.

In short, if you can make more money on your money in the relative short term lease it. If you can't and really want to enjoy it for a long time buy it and use the rest of the money to invest. It will depreciate for a long time but the longer you keep it the less value it will lose.

At any rate I hope what I said helps.

Last edited by George from MD; 06-09-2024 at 08:50 PM.

I've had a "car fund" for over 25 years. I only use it for non-depreciating toys. I don't need spousal approval for any purchase made with my car fund money (although I always discuss purchases with my wife as she is my sounding board in this regard). This money is kept in a separate US account and the account balance fluctuates as I buy or sell something. My goal with my car fund and those purchases is to not lose any of my capital over time as I consider it part of my retirement fund. Most often, I have a small gain on these toys, but I have hit a few home runs when collector car/bike markets have increased.

Any car that I am using as a daily, including my upcoming 992 summer car, is part of my annual "operating" budget. I use my LOC for these cars. I calculate my payment based on the length of time that I plan on keeping it. If it is a car that will be an 8 - 10 year car, I use current LOC interest rates and depreciate it fully over that period of time. There is always some equity left when I do this. On a car that I may keep for 4 or 5 years, I use a lease calculator and lease it to myself using a very conservative residual to ensure that I at least break even, but most often have equity left when I sell or trade it. When I get my annual bonus I usually apply a portion of it to the LOC cars, so most of them never stay on the LOC for the expected term. For example, my wife's 2017 RX350 payment was calculated using an 8 year pay-off. However, it was paid in full in 2020. I don't have a mortgage or any other debt, so my LOC is only for cars and I keep accurate monthly records on the residual value of each. If I can't afford the payment in my budget or don't feel that the monthly expense is worth it to me, I don't buy the car. I know some would say why would you take on debt when you have the cash available? I do this to ensure that I am living within my budget. If I just pay cash using my car fund for example, I will technically have more "budget" available and could talk myself into spending that budget - as many of my customers do each fall

As you can probably tell, I am not a finance guy and have little interest in finance. I also don't need to be the wealthiest guy on the block and I am not a prisoner to the concept that we all need $250k/year after tax to retire comfortably. I use software to manage my money - Quicken for the operating budget and Snap Projections to manage my retirement projections. Probably too much info for most, but I find it interesting to hear how others manage their expenses, so I thought I would share.

I also know some people that bought their P car from accessing their LOC or HELOC's. Rates are much lower using your secure LOC vs leasing and financing from the dealer.

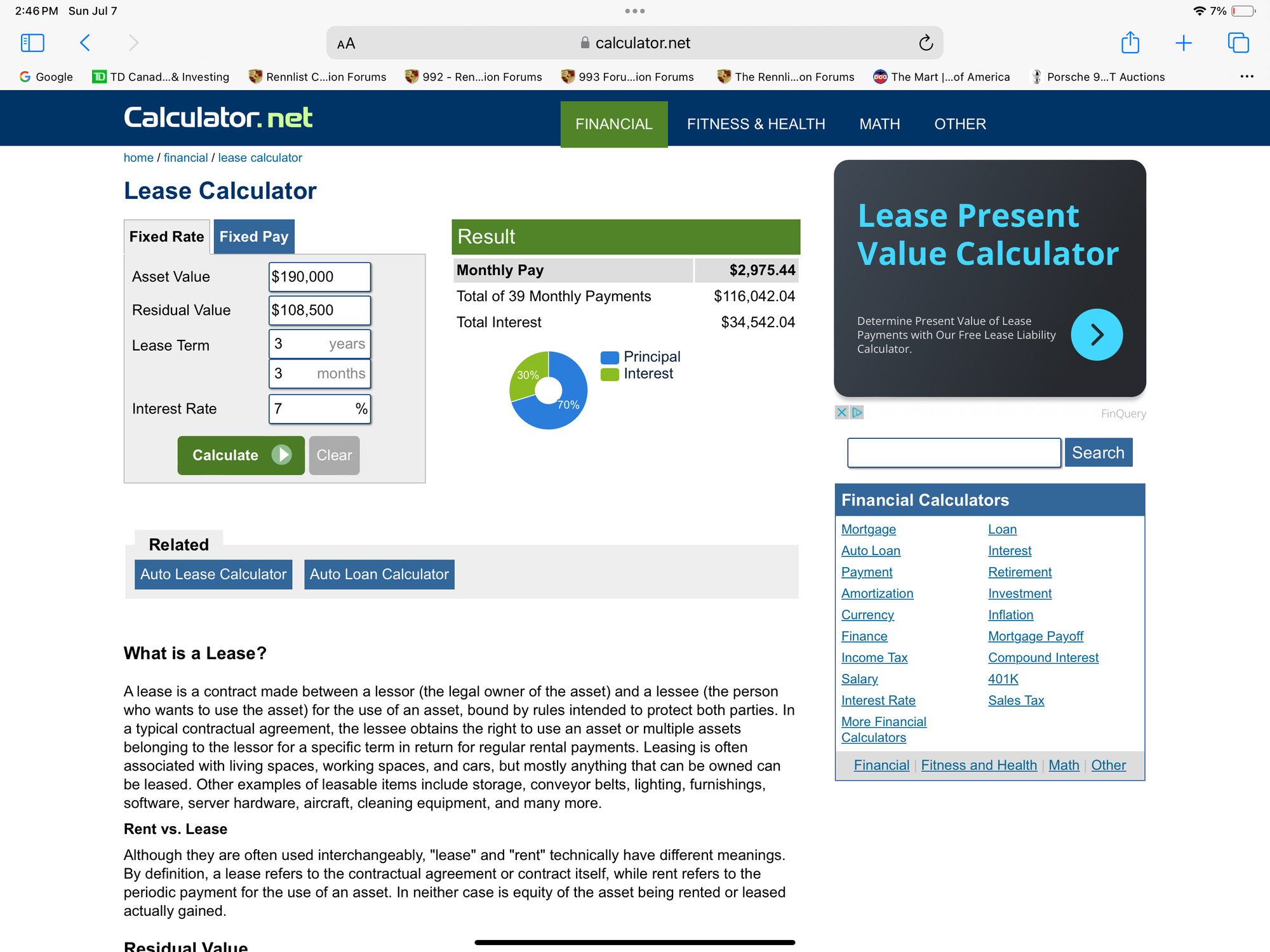

That residual is 57% of the $155k - that is where Porsche is making its money. This chart shows more real-world depreciation numbers. HELOC is 7.25% right now…likely 7% next month. You’ll save a lot of money buying vs leasing. Disregard the years on the right…this is just an estimate.

If I was looking at your Cayenne, I would use this lease calculation with a conservative 30% depreciation to come up with my monthly payment on my Heloc. If my numbers are correct, I’d save $15,466 this way.

let's say if a new 2025 Cayenne that was leased for 39 months, and the Cayenne got into accident and need lots of repairs during the 39 months period, will it affect the residual value of the leased Cayenne once lease is up?

One pros I see leasing expensive car is that if there is accident to the car during lease period, I do not have to be the final bag holder of depreciated value of car due to accident damage? Am I wrong or missing something?

let's say if a new 2025 Cayenne that was leased for 39 months, and the Cayenne got into accident and need lots of repairs during the 39 months period, will it affect the residual value of the leased Cayenne once lease is up?

One pros I see leasing expensive car is that if there is accident to the car during lease period, I do not have to be the final bag holder of depreciated value of car due to accident damage? Am I wrong or missing something?

yes that is one advantage. however in todays market there are many downsides to leasing such as the artifically low residuals (unless you plan on exercising at lease end) and high interest. Look at the example above, 34k over 3 years in interest alone with that 7%. We all have access to cheap money but in a lease you are forced into the OEM's financial divison rates.

Gone are the years of cheap leases. 4 out of my last 5 cars were purchased outright including both last year. 10 years ago it was the opposite.

let's say if a new 2025 Cayenne that was leased for 39 months, and the Cayenne got into accident and need lots of repairs during the 39 months period, will it affect the residual value of the leased Cayenne once lease is up?

One pros I see leasing expensive car is that if there is accident to the car during lease period, I do not have to be the final bag holder of depreciated value of car due to accident damage? Am I wrong or missing something?

I would rather pay the extra interest and have the ability to wash my hands of the car in 3 years if something were to happen to it.

Sometimes residuals are negotiable, But I may be thinking used cars.

I would rather pay the extra interest and have the ability to wash my hands of the car in 3 years if something were to happen to it.

Sometimes residuals are negotiable, But I may be thinking used cars.

With 9% in that Cayenne GTS example, interest is $1200 of the $3400 lease payment (33%!). Total lease obligation of 132k over 39 months. Even buying out the car at that time will come out to 245k total. Thats insanity. I'd absolutely run away from that. Is it worth that "if I get into an accident" peace of mind?

Coincidently I also almost pulled the trigger on a 155k 2023 Cayenne GTS . Bought a 140k RS6 instead. Holding for 3 years and selling will net me 1000$ monthy cost. Thats 93k less over 3 years for 15k MSRP difference up front.

Last edited by Maitre_Absolut; 07-10-2024 at 05:02 PM.

With 9% in that Cayenne GTS example, interest is $1200 of the $3400 lease payment (33%!). Total lease obligation of 132k over 39 months. Even buying out the car at that time will come out to 245k total. Thats insanity. I'd absolutely run away from that. Is it worth that "if I get into an accident" peace of mind?

Coincidently I also almost pulled the trigger on a 155k 2023 Cayenne GTS . Bought a 140k RS6 instead. Holding for 3 years and selling will net me 1000$ monthy cost. Thats 93k less over 3 years for 15k MSRP difference up front.

I totally agree with you. I don't see the point of spending that much money on a Cayenne in general lol

But my point is I can use $245 give or take on a down payment for a building that I can lease out and make more than $ 3400/ month that could pay for whatever I want.

06-09-2024, 07:56 PM

06-09-2024, 07:56 PM