No more ADM‘s/ Prices lowering

Rennlist Member

Joined: Mar 2018

Posts: 573

Likes: 535

From: Rolling Hills Estates, CA

Three Wheelin'

Joined: Jun 2017

Posts: 1,703

Likes: 2,682

From: Arizona

The difference is Brexit. That really knecapped Great Britain and their entire economy is a mess. The wealthy have been hurt too which is Porsche's target market.

"The average Briton was nearly Ł2,000 worse off in 2023, while the average Londoner was nearly Ł3,400 worse off last year as a result of Brexit, the report reveals. It also calculates that there are nearly two million fewer jobs overall in the UK due to Brexit – with almost 300,000 fewer jobs in the capital alone.

https://www.london.gov.uk/new-report...apital%20alone.

"The average Briton was nearly Ł2,000 worse off in 2023, while the average Londoner was nearly Ł3,400 worse off last year as a result of Brexit, the report reveals. It also calculates that there are nearly two million fewer jobs overall in the UK due to Brexit – with almost 300,000 fewer jobs in the capital alone.

https://www.london.gov.uk/new-report...apital%20alone.

Racer

Joined: Dec 2023

Posts: 389

Likes: 282

Rennlist Member

Joined: Feb 2006

Posts: 1,218

Likes: 516

From: Long Grove, IL

I bought a nearly new base 911 (sticker was $137k) w 3,000 miles and CPO for $134k 2 months ago. The dealer had it for sale for 4 months. When I was hunting for a car it was wild how prices were all over the place and how some dealers had cars on their lots for 6 months.

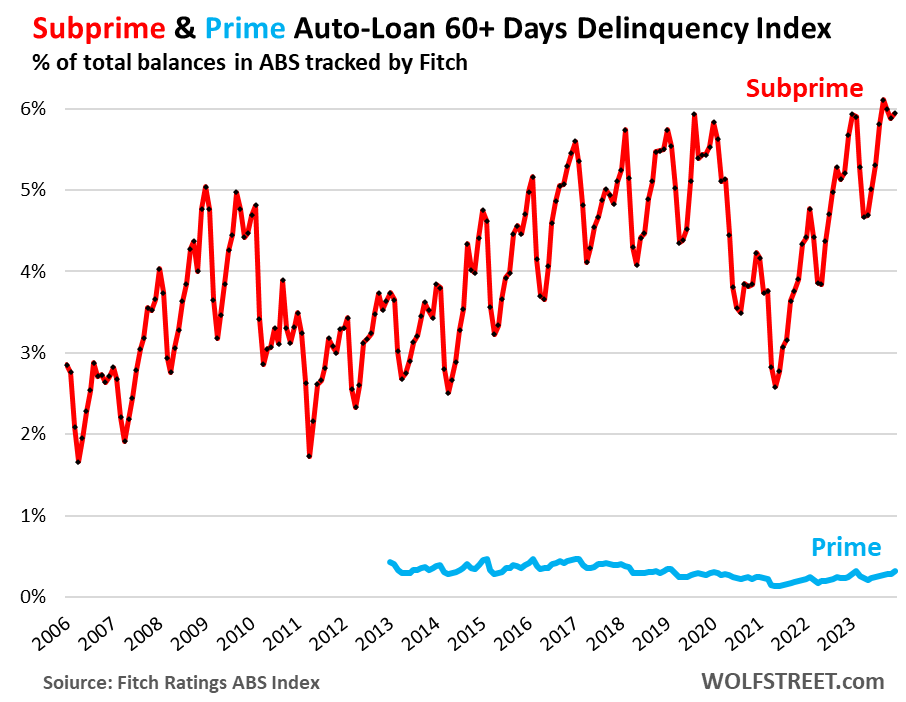

With car payment delinquencies at 30 year high banks are starting to tighten up lending standards… add high floor plan rates and the eco failure around the electric cars, the car business feels like the housing market in 2008…. Will be interesting to see how the year plays out.

With car payment delinquencies at 30 year high banks are starting to tighten up lending standards… add high floor plan rates and the eco failure around the electric cars, the car business feels like the housing market in 2008…. Will be interesting to see how the year plays out.

You are perhaps referring to sub prime car loans? I saw a report on Forbes that made the same misleading blanket statement and the actual truth was buried in the story. FYI, subprimes make up less than 15% of car loans.

Borrowers with prime credit scores are responsible for the majority of retail vehicle financing. Borrowers with credit scores of 661 and higher account for 68.5% of retail vehicle financing, according to Experian, versus 14.5% for subprime borrowers with credit scores of 600 or lower.

Primes are doing fine, as has been the case historically. no need to panic. OTOH sub prime loans are a terrible way to finance and the companies making them are often predatory. Sucks to be in an economic bind in the USA for sure but many subprime lenders deserve a special level of hell.

https://www.lendingtree.com/auto/deb...0%20or%20lower.

Instructor

Joined: Dec 2023

Posts: 102

Likes: 74

In my market there was only one dealer that was charging ADM for all models (base, S etc). All other dealers were no ADM from the start for all cars except GT models including GTS. But with allocation you could have ordered base, S, 4 etc at MSRP since the 992 was introduced. Meanwhile since November-December, the one dealer that was asking for ADM also dropped the ADM, and the allocations became available much quicker. Either Porsche increased the production, or those who were in the lists dropped off or didn't want allocations.

Meanwhile the CPO cars are so hard to come by, dealers are selling them over MSRP any day of the week.

Meanwhile the CPO cars are so hard to come by, dealers are selling them over MSRP any day of the week.

Rennlist Member

Joined: Jan 2011

Posts: 1,347

Likes: 431

From: NJ

You are perhaps referring to sub prime car loans? I saw a report on Forbes that made the same misleading blanket statement and the actual truth was buried in the story. FYI, subprimes make up less than 15% of car loans.

Borrowers with prime credit scores are responsible for the majority of retail vehicle financing. Borrowers with credit scores of 661 and higher account for 68.5% of retail vehicle financing, according to Experian, versus 14.5% for subprime borrowers with credit scores of 600 or lower.

Primes are doing fine, as has been the case historically. no need to panic. OTOH sub prime loans are a terrible way to finance and the companies making them are often predatory. Sucks to be in an economic bind in the USA for sure but many subprime lenders deserve a special level of hell.

https://www.lendingtree.com/auto/deb...0%20or%20lower.

Borrowers with prime credit scores are responsible for the majority of retail vehicle financing. Borrowers with credit scores of 661 and higher account for 68.5% of retail vehicle financing, according to Experian, versus 14.5% for subprime borrowers with credit scores of 600 or lower.

Primes are doing fine, as has been the case historically. no need to panic. OTOH sub prime loans are a terrible way to finance and the companies making them are often predatory. Sucks to be in an economic bind in the USA for sure but many subprime lenders deserve a special level of hell.

https://www.lendingtree.com/auto/deb...0%20or%20lower.

Racer

Joined: Dec 2011

Posts: 314

Likes: 139

From: Northern Virginia, USA

I can see the EV 911 being 20% more, but not a hybrid. We're still far off from the EV 911 launch. I believe I read the Boxster/Cayman EV is going to be 20% more than the ICE versions.

Racer

Joined: Dec 2011

Posts: 314

Likes: 139

From: Northern Virginia, USA

Thinking of doing the same with my Audi A8L. Just have Carvana take it off my hands for the KBB price. Not dealing with traditional dealers on trades. You never get a decent offer it seems.

Drifting

Joined: Oct 2020

Posts: 2,925

Likes: 2,259

From: Alberta/BC

My dealer without asking gave me a Ctek, a bunch of Porsche swag (I use the thermos cup everyday) and not once did they mention any upsell of anything. The finance office's only question was cheque still or do you want to finance? The cost of the car was MSRP + tax. No hidden BS. Cleanest sales process I've ever seen when it came time to sign the paperwork.

Three Wheelin'

Joined: Feb 2012

Posts: 1,300

Likes: 844