When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

There was a recent thread about raised car insurance, I received my house insurance renew a few days ago, my (pre-tax) annual premium jumped from $485 to $852, a 75% increase !

This is without any claim history over the last 16 years.

The premium two years ago was $635.

Anybody experienced similar?

I called the insurance company today, the agent was surprised as well, she verified I had all possible discounts in place, then put me on hold, came back to tell me the increase is because the postal code my house is at, but could only suggest there was probably more claim recently which caused this increase.

I asked her if it's because of the ice storm last year? She doesn't know, although I told her there was hardly any damage that I saw around my area, doesn't support her suggestion......

Dollar figure is totally irrelevant here since there are so many variables. House size, fireplace, accessories, location etc.

Mine went up about 12% last November.

I think replacement value on the structure as well as valuables plays a big part in pricing as well as location (recent flooding in area, high crime etc...)

Adam is your house and property worth 600k or just the building as that is what they are insuring? the property will always be there so they only insure replacement of the building. also contents such as jewellery is a big factor which you did not include.

Adam is your house and property worth 600k or just the building as that is what they are insuring? the property will always be there so they only insure replacement of the building. also contents such as jewellery is a big factor which you did not include.

Sorry, the house and property is 600k. House replacement value on my policy is 480k.

I don't have any specific contents on my policy, no major stashes of jewellery.

FYI when I put the lift in I notified them and it had no effect.

I had an interesting discussion with a State Farm broker last year and I basically wrestled him to the ground and had him admit that house insurance is the new banking scam being set up by the insurance industry. They are using new metrics of auto insurance 'risk' to apply to house insurance and where none of this increased risk is really factual.

Many of the 'losses' the insurance industry *say* that they have experienced, (the excuse for why they raise rates) has nothing to do with either auto or housing losses - it has everything to do with their market investment losses.

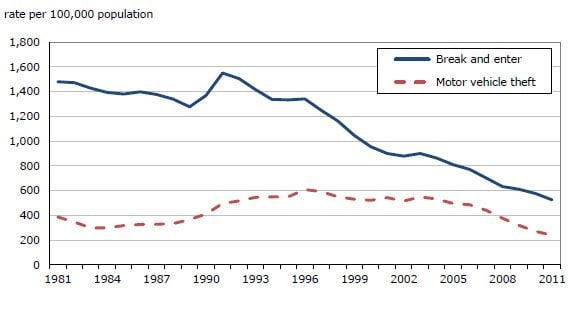

The police break and enter reports - the fire department reports - all public documents, tell a different story than what the insurance industry portray. All show fewer fires (and why Fire dept's are under the gun to downsize and pressure to hire more EMT's) while break and enter losses have FALLEN over all.

(Stat Canada)

The public data doesn't match the story they are telling.

Its all a shell game and the Province and the industry know it. The industry tells the Government there is an increase in risk - the Government does no investigation of these claims and allows increases because of the exceptionally great lobby efforts on behalf of this industry.

The Government can say they 'held' increases down - well except for the increase you got in the mail - that doesn't count they say - then the industry points their fingers at a few Tamils or a stupid plumber burning down an under construction set of town houses and everyone is happy.

Now we have insurance companies heavily invested in the commercial real estate market, (after being burned in the derivative markets) and that market isn't doing so well... I smell another rate increase.

We pay high fees because the insurance industry have idiots running their investment portfolio departments. What a great little scam they have going on here. What other investor has this great well of funds to keep dipping into when they lose their shirts in the markets or because buildings they bought at too high a price aren't leasing so well?

What other industry has a legislated 20% (minimum) return guaranteed by Government on top of their costs? So if you can pad your costs...

I noticed my house insurance rate increased. When discussing with my broker I realized that you should never make a claim on your house insurance unless it is a big claim (at least 20k). If you make a first claim the second one could get your policy cancelled or big increase. So I decided to increase my deductible which lowered my premiums. This makes a lot of sense to me.

02-19-2015, 10:45 PM

02-19-2015, 10:45 PM